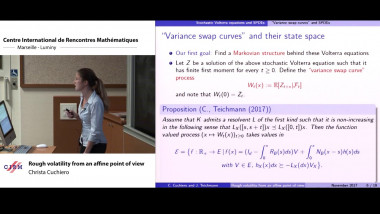

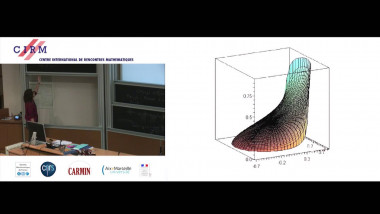

Rough volatility from an affine point of view

Apparaît également dans la collection : Advances in stochastic analysis for risk modeling / Avancées en analyse stochastique pour la modélisation des risques

We represent Hawkes process and their Volterra long term limits, which have recently been used as rough variance processes, as functionals of infinite dimensional affine Markov processes. The representations lead to several new views on affine Volterra processes considered by Abi-Jaber, Larsson and Pulido. We also discuss possible extensions to rough covariance modeling via Volterra Wishart processes. The talk is based on joint work with Josef Teichmann.

![$k$-sum free sets in $[0,1]$](/media/cache/video_light/uploads/video/2015-09-10_de_Roton-video--19cf70874d3c5af7378c268cab865b06.jpg)